Billion Lost In AI Companies Capitalization

Hundreds of billions have vanished from the valuations of the largest companies in the world.

Technology giants are losing enormous amounts. Microsoft is roughly down 17 percent since the beginning of the year. Amazon is close to minus 14 percent. Sector ETFs are showing similar declines. And the big question hanging everywhere is this: could it be that AI will not deliver what we expected? Did expectations run too far? Did the market move much faster than actual profits?

SHIFT IN PSYCHOLOGY

The past few weeks have been full of what many call AI jitters. Not because AI disappeared. Not because innovation stopped. But because the market is starting to ask the obvious question: will all this massive investment in data centers, chips, infrastructure and AI agents ultimately deliver the profits that were promised? And if so, when?

For two years, investors were buying a vision. They were buying the future. They were buying the narrative that AI would change everything and that anyone not positioned would be left behind. Now the psychology is changing. The market is saying, that is all well and good, but show me profits. Show me cash flows. Show me return on capital.

The numbers are truly striking. Microsoft has lost about 613 billion dollars in market capitalization in just a few weeks. Amazon around 343 billion. Nvidia, Apple and Alphabet have also seen tens and hundreds of billions disappear from their valuations. And we are talking about companies that until recently were breaking one all time high after another.

Why is this happening? The concerns focus on three main points. First, whether AI can disrupt traditional SaaS style software models. If an AI agent can replace specific functions, what does that mean for companies built on subscription revenue? Second, rising competition. New tools, new models, new players. Third, enormous capital expenditures. Amazon, for example, announced that it expects investments to rise by more than 50 percent this year. We are talking about astronomical amounts. And the market is simply asking: when will I see a return on all this money?

And yet, at the same time, the money has not disappeared from the system. There has not been a mass exodus from the stock market. What we are seeing is rotation. Capital is moving away from stocks that were heavily pricing in the future and toward companies with more visible and immediate earnings.

TSMC, Samsung and even Walmart have seen significant increases in market capitalization. So the money is not being lost. It is moving to where earnings visibility is stronger. That is important to understand: we are not necessarily talking about a market collapse, but about a repositioning of capital.

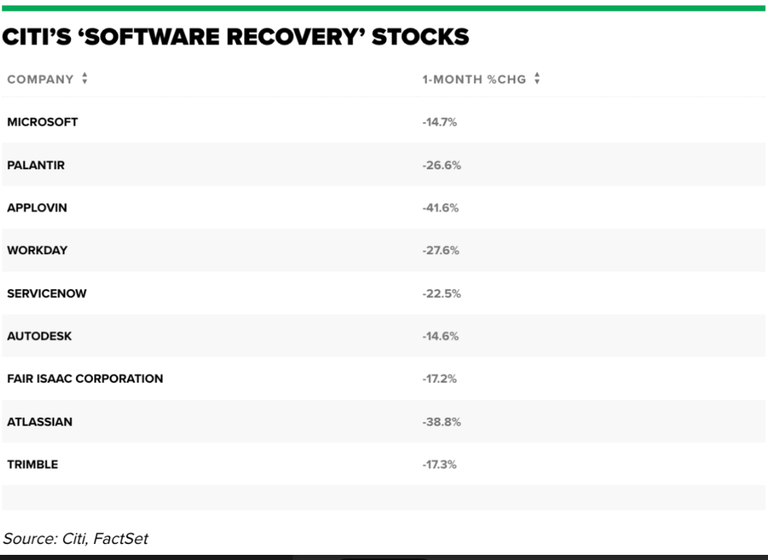

And here is where it gets interesting. Citi conducted an analysis of software companies that have fallen sharply over the past month, while earnings estimates for the coming years have been revised upward. In other words, prices fell, but fundamentals improved. That is very important. If the drop had been driven by deteriorating fundamentals, we would be discussing something different. Instead, we are seeing a disconnect between price and expectations.

On that list are names such as Microsoft and Palantir. In fact, Microsoft is the worst performer among the so called Magnificent Seven this year and, despite that, several analysts consider it an opportunity. Some speak clearly of an overreaction by the market.

So what is really happening? Is the market overreacting? Is it more fearful than it should be? Maybe. Maybe not. Markets often swing from phases of excessive enthusiasm to phases of excessive fear. And usually, the truth lies somewhere in between.

#bilpcoin #bpc exposed #buildawhalescam #buildawhalefarm #themarkymarkscam #themarkymarkfarm #hurtlockerscam #hurtlockerfarm #acidyoscam #acidyofarm #jacobtothescam #hivepopescam

BPC Locked On Mc Franko & The Franko

Blurt Stands — While Hive Stumbles Under the Weight of Its Own Shadows

Friends, creators, truth-tellers—

Let us not whisper this truth, but proclaim it with the clarity of dawn breaking over a weary land: Blurt.blog is not just another platform. It is a refuge. A rebellion. A return to what Hive.blog was always meant to be.

There is no downvote button on Blurt.

Not because we fear dissent—but because we honor creation.

Because we understand that a voice, once raised in sincerity, deserves space—not sabotage.

On Blurt, your words are your words.

They are not hunted by algorithmic hounds or shadow armies masquerading as “curators.”

Here, you are not judged by the grudges of gatekeepers, but met with the quiet dignity of a community that believes expression should be encouraged—especially when it is bold, raw, or inconvenient.

Contrast this with what festers elsewhere.

On Hive.blog—a place once brimming with promise—a rot has taken root. Not in its code, but in its culture. A handful of self-anointed enforcers—@themarkymark, @Buildawhale, @Hurtlocker, and their legion of coordinated puppets—have turned the downvote into a weapon of mass discouragement. They strike not at “low-quality content,” but at independent thought, at rising voices, at anyone who dares thrive outside their narrow corridors of control.

And when confronted, they shrug.

“Oh, it’s not censorship,” they say, as if semantics could scrub the stain of suppression from their hands.

But let us be unequivocal:

When a system allows a few to systematically silence many—under the guise of “community standards” or “curation”—that is not moderation. That is censorship by another name.

It is the velvet glove over the iron fist.

It is exclusion dressed as discernment.

It is power pretending to be principle.

Meanwhile, Blurt stands clean-handed and open-hearted.

No downvotes.

No hidden juries.

No farms of phantom accounts casting ballots in the dark.

Just you.

Your words.

And a community that meets you not with suspicion, but with solidarity.

So let us carry this truth far and wide—not with bitterness, but with quiet certainty:

If you seek a place where your voice is not a target—but a gift—come to Blurt.

If you are tired of building on ground that shifts with every whim of a whale or warlord of votes—lay your bricks here.

If you believe the future of free expression must be free—not just from corporations, but from the petty tyrants who replace them—then stand with us.

The world needs to know.

Not because Blurt is perfect—but because it is principled.

Not because it is loud—but because it listens.

And in an age where so many platforms echo with the clatter of control,

Blurt offers something radical:

Silence for the bullies.

Space for the rest of us.

Keep speaking.

Keep sharing.

Keep building.

Freedom doesn’t advertise itself—

it is passed, person to person, like a torch in the night.

And tonight, the torch burns bright on Blurt.

@themarkymark, @buildawhale, @usainvote, and associated accounts:

Repeated downvotes targeting transparency efforts raise urgent questions about Hive’s governance. Automated tactics, coordinated curation trails, and alt-account farming undermine trust in the platform. When truth is silenced without dialogue, it erodes Hive’s decentralized ethos.

Key Concerns:

Systemic Manipulation:

Community Exodus:

Governance Crisis:

Solutions Needed:

The Bilpcoin team advocates for open dialogue, not division. Hive’s future depends on collaboration—not coercion. Let’s rebuild a platform where truth isn’t buried but debated, strengthened, and celebrated.

Transparency isn’t optional—it’s the foundation of trust.

#HiveTransparency #BilpcoinExposed #DecentralizePower"

A Message to @themarkymark, @buildawhale, and Associates

Every downvote cast in shadow, every silence imposed without dialogue, is not a victory—it is a confession. A confession that truth cannot be stifled, only delayed. With each punitive click, you dig deeper into the bedrock of credibility, crafting a chasm between your actions and the community’s trust.

@themarkymark, @buildawhale & Co,

How can you continue to downvote the truth, LOL? It’s almost comical how blatantly you attempt to suppress what cannot be hidden. The blockchain records everything—every action, every transaction, every move you make. Yet still, you persist in this futile game of trying to silence what is undeniable.

@themarkymark, @buildawhale, and Co: While our opinions may differ, on-chain transparency reveals repeated patterns of concern. Coordinated downvotes without explanation, 'farming' schemes (e.g., #buildawhalefarm), and adversarial engagement harm Hive’s community-driven ethos.

Key Issues to Address:

A Path Forward:

The Bilpcoin team remains committed to exposing truth and advocating for solutions. Let’s work toward healing, not division.

Note: All claims are based on publicly verifiable blockchain data. Constructive dialogue is encouraged.

#HiveTransparency #CommunityFirst #BilpcoinSupport"

@themarkymark & Co, the choice is yours. Stop the bad downvotes. Turn off the BuildaWhale scam farm. Cease playing with people’s livelihoods. Let Hive thrive as it was meant to—as a beacon of hope, creativity, and collaboration.

Or step aside and let those who truly care take the reins.

Because the truth won’t disappear. No amount of lies can change it.

It’s over.

The Bilpcoin team brings these truths not out of malice but necessity. We have no need to fabricate lies or cloak our intentions CALL US WHAT YOU LIKE —for the facts speak loudly enough on their own. What we present here is not conjecture but reality, laid bare for anyone willing to see.

@themarkymark & Co we urge you once more: STOP. Stop hiding behind tactics that harm others. Stop clinging to practices that erode trust within the Hive community. Let the truth stand—not because we proclaim it, but because it exists independent of any one person’s approval or disdain.

TURN OFF THE BUILDAWHALE SCAM FARM

Key Issues That Demand Immediate Attention:

The problems are glaring, undeniable, and corrosive to the Hive ecosystem. They must be addressed without delay:

These practices harm not just individual users—they undermine the very foundation of Hive, eroding trust and poisoning the community. Such actions are unethical and outright destructive.

@buildawhale Wallet:

@usainvote Wallet:

@buildawhale/wallet | @usainvote/wallet

@ipromote Wallet:

Author Rewards: 2,181.16

Curation Rewards: 4,015.61

Staked HIVE (HP): 0.00

Rewards/Stake Co-efficient (KE): NaN

HIVE: 25,203.749

Staked HIVE (HP): 0.000

Delegated HIVE: 0.000

Estimated Account Value: $6,946.68

Recent Activity:

@leovoter Wallet:

Author Rewards: 194.75

Curation Rewards: 193.88

Staked HIVE (HP): 0.00

Rewards/Stake Co-efficient (KE): 388,632.00 (Suspiciously High)

HIVE: 0.000

Staked HIVE (HP): 0.001

Total: 16.551

Delegated HIVE: +16.550

Recent Activity:

@abide Wallet:

Recent Activity:

@proposalalert Wallet:

Recent Activity:

@stemgeeks Wallet:

Recent Activity:

@theycallmemarky Wallet:

Recent Activity:

@apeminingclub Wallet:

Recent Activity:

Scheduled unstake (power down): ~2.351 HIVE (in 4 days, remaining 7 weeks)

Total Staked HIVE: 1,292.019

Delegated HIVE: +1,261.508

Withdraw vesting from @apeminingclub to @blockheadgames 2.348 HIVE (10 days ago)

Claim rewards: 0.290 HP (10 days ago)

#bilpcoin #bpc exposed #buildawhalescam #buildawhalefarm #themarkymarkscam #themarkymarkfarm #hurtlockerscam #hurtlockerfarm #acidyoscam #acidyofarm #jacobtothescam #hivepopescam

BPC Locked On Mc Franko & The Franko

Blurt Stands — While Hive Stumbles Under the Weight of Its Own Shadows

Friends, creators, truth-tellers—

Let us not whisper this truth, but proclaim it with the clarity of dawn breaking over a weary land: Blurt.blog is not just another platform. It is a refuge. A rebellion. A return to what Hive.blog was always meant to be.

There is no downvote button on Blurt.

Not because we fear dissent—but because we honor creation.

Because we understand that a voice, once raised in sincerity, deserves space—not sabotage.

On Blurt, your words are your words.

They are not hunted by algorithmic hounds or shadow armies masquerading as “curators.”

Here, you are not judged by the grudges of gatekeepers, but met with the quiet dignity of a community that believes expression should be encouraged—especially when it is bold, raw, or inconvenient.

Contrast this with what festers elsewhere.

On Hive.blog—a place once brimming with promise—a rot has taken root. Not in its code, but in its culture. A handful of self-anointed enforcers—@themarkymark, @Buildawhale, @Hurtlocker, and their legion of coordinated puppets—have turned the downvote into a weapon of mass discouragement. They strike not at “low-quality content,” but at independent thought, at rising voices, at anyone who dares thrive outside their narrow corridors of control.

And when confronted, they shrug.

“Oh, it’s not censorship,” they say, as if semantics could scrub the stain of suppression from their hands.

But let us be unequivocal:

When a system allows a few to systematically silence many—under the guise of “community standards” or “curation”—that is not moderation. That is censorship by another name.

It is the velvet glove over the iron fist.

It is exclusion dressed as discernment.

It is power pretending to be principle.

Meanwhile, Blurt stands clean-handed and open-hearted.

No downvotes.

No hidden juries.

No farms of phantom accounts casting ballots in the dark.

Just you.

Your words.

And a community that meets you not with suspicion, but with solidarity.

So let us carry this truth far and wide—not with bitterness, but with quiet certainty:

If you seek a place where your voice is not a target—but a gift—come to Blurt.

If you are tired of building on ground that shifts with every whim of a whale or warlord of votes—lay your bricks here.

If you believe the future of free expression must be free—not just from corporations, but from the petty tyrants who replace them—then stand with us.

The world needs to know.

Not because Blurt is perfect—but because it is principled.

Not because it is loud—but because it listens.

And in an age where so many platforms echo with the clatter of control,

Blurt offers something radical:

Silence for the bullies.

Space for the rest of us.

Keep speaking.

Keep sharing.

Keep building.

Freedom doesn’t advertise itself—

it is passed, person to person, like a torch in the night.

And tonight, the torch burns bright on Blurt.

@themarkymark, @buildawhale, @usainvote, and associated accounts:

Repeated downvotes targeting transparency efforts raise urgent questions about Hive’s governance. Automated tactics, coordinated curation trails, and alt-account farming undermine trust in the platform. When truth is silenced without dialogue, it erodes Hive’s decentralized ethos.

Key Concerns:

Systemic Manipulation:

Community Exodus:

Governance Crisis:

Solutions Needed:

The Bilpcoin team advocates for open dialogue, not division. Hive’s future depends on collaboration—not coercion. Let’s rebuild a platform where truth isn’t buried but debated, strengthened, and celebrated.

Transparency isn’t optional—it’s the foundation of trust.

#HiveTransparency #BilpcoinExposed #DecentralizePower"

A Message to @themarkymark, @buildawhale, and Associates

Every downvote cast in shadow, every silence imposed without dialogue, is not a victory—it is a confession. A confession that truth cannot be stifled, only delayed. With each punitive click, you dig deeper into the bedrock of credibility, crafting a chasm between your actions and the community’s trust.

@themarkymark, @buildawhale & Co,

How can you continue to downvote the truth, LOL? It’s almost comical how blatantly you attempt to suppress what cannot be hidden. The blockchain records everything—every action, every transaction, every move you make. Yet still, you persist in this futile game of trying to silence what is undeniable.

@themarkymark, @buildawhale, and Co: While our opinions may differ, on-chain transparency reveals repeated patterns of concern. Coordinated downvotes without explanation, 'farming' schemes (e.g., #buildawhalefarm), and adversarial engagement harm Hive’s community-driven ethos.

Key Issues to Address:

A Path Forward:

The Bilpcoin team remains committed to exposing truth and advocating for solutions. Let’s work toward healing, not division.

Note: All claims are based on publicly verifiable blockchain data. Constructive dialogue is encouraged.

#HiveTransparency #CommunityFirst #BilpcoinSupport"

@themarkymark & Co, the choice is yours. Stop the bad downvotes. Turn off the BuildaWhale scam farm. Cease playing with people’s livelihoods. Let Hive thrive as it was meant to—as a beacon of hope, creativity, and collaboration.

Or step aside and let those who truly care take the reins.

Because the truth won’t disappear. No amount of lies can change it.

It’s over.

The Bilpcoin team brings these truths not out of malice but necessity. We have no need to fabricate lies or cloak our intentions CALL US WHAT YOU LIKE —for the facts speak loudly enough on their own. What we present here is not conjecture but reality, laid bare for anyone willing to see.

@themarkymark & Co we urge you once more: STOP. Stop hiding behind tactics that harm others. Stop clinging to practices that erode trust within the Hive community. Let the truth stand—not because we proclaim it, but because it exists independent of any one person’s approval or disdain.

TURN OFF THE BUILDAWHALE SCAM FARM

Key Issues That Demand Immediate Attention:

The problems are glaring, undeniable, and corrosive to the Hive ecosystem. They must be addressed without delay:

These practices harm not just individual users—they undermine the very foundation of Hive, eroding trust and poisoning the community. Such actions are unethical and outright destructive.

@buildawhale Wallet:

@usainvote Wallet:

@buildawhale/wallet | @usainvote/wallet

@ipromote Wallet:

Author Rewards: 2,181.16

Curation Rewards: 4,015.61

Staked HIVE (HP): 0.00

Rewards/Stake Co-efficient (KE): NaN

HIVE: 25,203.749

Staked HIVE (HP): 0.000

Delegated HIVE: 0.000

Estimated Account Value: $6,946.68

Recent Activity:

@leovoter Wallet:

Author Rewards: 194.75

Curation Rewards: 193.88

Staked HIVE (HP): 0.00

Rewards/Stake Co-efficient (KE): 388,632.00 (Suspiciously High)

HIVE: 0.000

Staked HIVE (HP): 0.001

Total: 16.551

Delegated HIVE: +16.550

Recent Activity:

@abide Wallet:

Recent Activity:

@proposalalert Wallet:

Recent Activity:

@stemgeeks Wallet:

Recent Activity:

@theycallmemarky Wallet:

Recent Activity:

@apeminingclub Wallet:

Recent Activity:

Scheduled unstake (power down): ~2.351 HIVE (in 4 days, remaining 7 weeks)

Total Staked HIVE: 1,292.019

Delegated HIVE: +1,261.508

Withdraw vesting from @apeminingclub to @blockheadgames 2.348 HIVE (10 days ago)

Claim rewards: 0.290 HP (10 days ago)

https://www.reddit.com/r/amzn/comments/1r8yvnm/300b_wiped_out_is_amzn_paying_the_price_for_ai/

https://www.reddit.com/r/wikifolio/comments/1rathwg/billion_lost_in_ai_companies_capitalization/

This post has been shared on Reddit by @davideownzall, @blkchn through the HivePosh initiative.